Think of it as paying for my salary.

The speaker? A teacher in Saskatoon, in December 1980 or January 1981.

The speakees? Recently relocated Albertans, chafing under the unaccustomed weight of a provincial sales tax.

The logic? The Government of Saskatchewan had presented the latest increase to said sales tax as a health-and-education surcharge. The subtext wasn’t subtle.

Be cheery when you pay this:

It’s for good stuff.

For a government trying to justify a specific tax or an increase thereto, it’s tempting to connect it–Somehow! Anyhow!–to an equally specific program expenditure of which most people will mostly approve. The Government of Saskatchewan merely waved a hand and said it was so; the following extract from an American site illustrates the same approach buttressed by a user-pay logic (although it slips a bit at the end when it refers to “other government infrastructure,” like that makes sense).

A gas tax is commonly used to describe the variety of taxes levied on gasoline at both the federal and state levels, to provide funds for highway repair and maintenance, as well as for other government infrastructure projects.

– Tax Foundation

Why are we here? Because a friend shared an article about the tax implications of replacing fossil-fuel-powered vehicles with zero-emission vehicles. In short: Where will the money come from to build and maintain our roads if we don’t have fossil fuels to kick around any more?

Well, it will come from somewhere else. Tax revenue is one pot of money. To do anything else–to account for and to sequester funds for a specified purpose–would be complex and inflexible. How we sell or justify or come to terms with a tax–that’s one thing. What we use the money for–that’s another.

Will we pay a “road surcharge” for electricity used to charge our cars? Maybe. Will we make up the difference by paying more taxes somewhere else? Maybe. Will we run deficits that effectively make future taxpayers pay for some of it? Maybe. Will we do all of the above? Maybe. And how much are we talking about, anyway–either the gas tax as she is now or the cost of highway infrastructure? Maybe. I mean, I have no idea.

I have a mild interest in governance, but I have somehow managed to get to 71-almost-72 with essentially no knowledge of the scale of the sources and uses of government funds at any level (federal, provincial, or municipal).

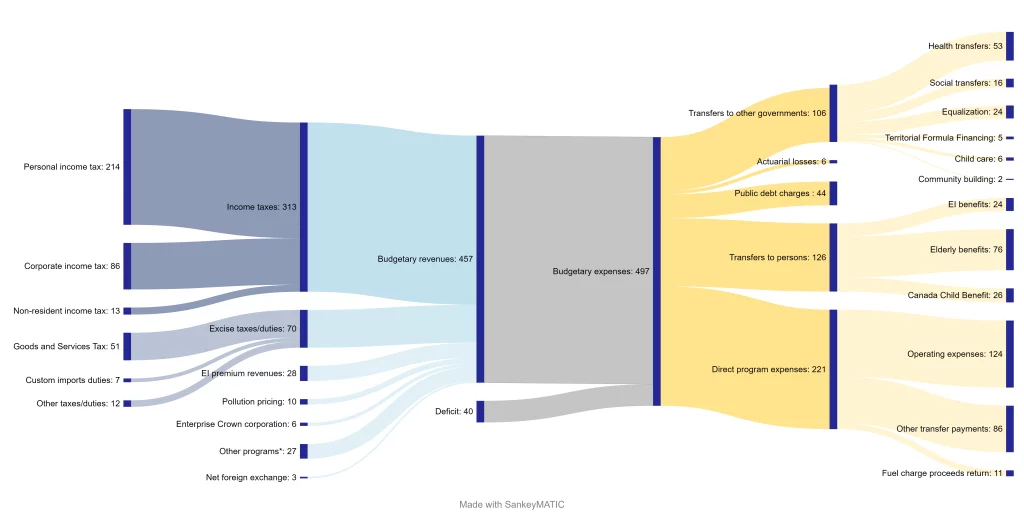

As part of an exciting taxpayer-funded series–Quick Reads on Canadian Topics–the feds published The 2023 Federal Budget at a Glance. I believe they’re overestimating my ability to apprehend stuff at a glance, but I’ll allow that it is more glance-ish than the actual budget, which clocks in at 266 pages. Here’s the centrepiece of the short version, which nicely upholds my “one pot of money” assertion. Note how that Deficit: 40 (Billion Dollars! Just sayin’!) quietly hangs there on the bottom in a don’t-look-at-me colour. Coincidence? Maybe.

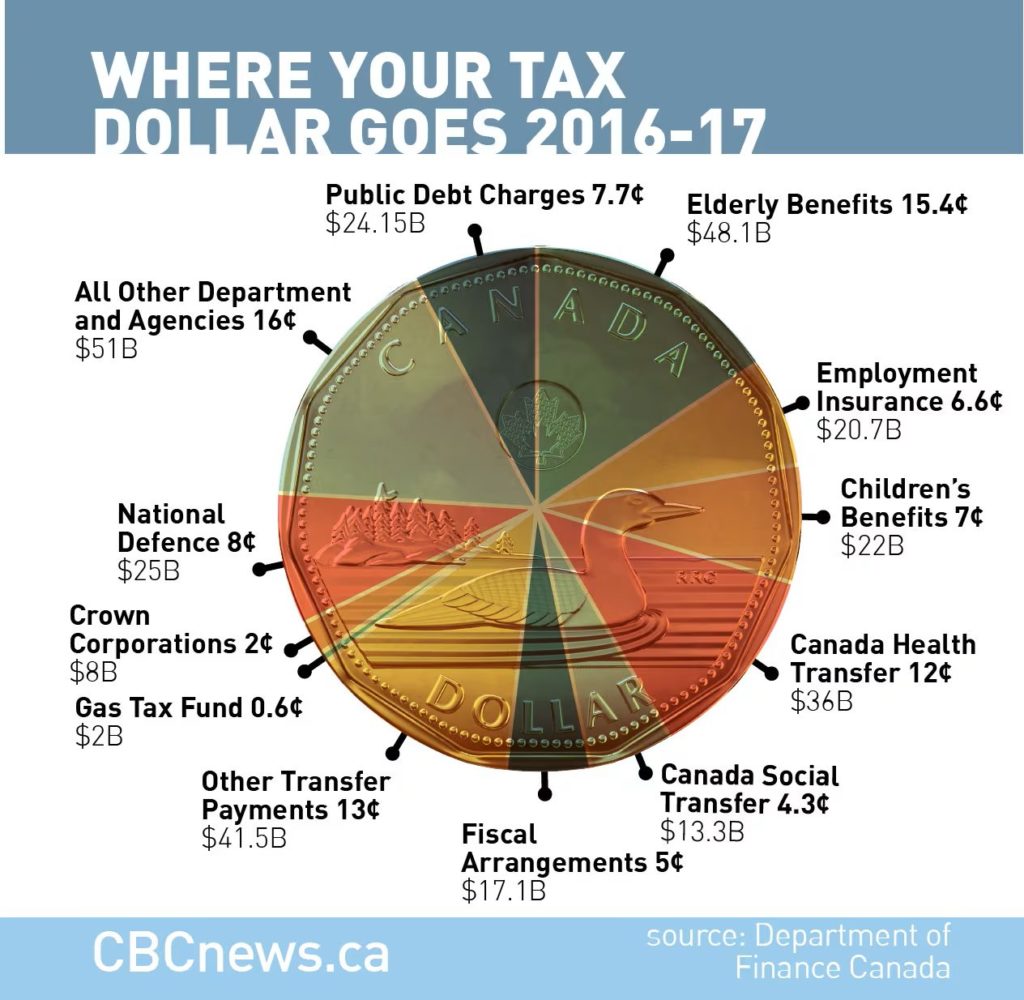

I’d respectfully suggest that, glance-wise, a pie chart might be better. The only one I could find was a CBC publication of a Department-of-Finance construct from 2016-2017.

The Department doesn’t seem to be doing this anymore. Because that would make it too easy to compare spending, year to year? Maybe. So let’s do it anyway, even though the categories aren’t all the same.

I see that Public Debt Charges have risen from $24 billion in 2016-17 to $44 billion in 2023-24. (They’re now forecast to be $52 billion next year, just edging out Health Transfers [feds to provinces/territories], oh, hurray). I also see that Elderly Benefits have risen from $48 billion to $76 billion over the same period. I was not a senior in 2016-17 and I am now, but I’m not sure that’s what’s drove this increase.

Anyway. Back to the point, which is . . . what? That this is too complicated for humans? Maybe. It’s too complicated for me, that’s for sure.

But here’s the thing, and yes, I can hear that faint cheering from the back of the hall as you sense this wrapping up. Settle down. The thing is this: The complexity of our tax-&-spend system and the inconstancy of the reporting thereon are, I fear, not bugs but features. That is, they are not accidental, they are intentional. Those who tax and spend have zero incentive to make this simple and clear and readily comparable year-to-year, and every incentive to make it complex and obscure and impossible to track.

Can we have better? Maybe. But only if we insist. And maybe not even then.

My personal take-away? It’s that time of year again when the self-employed-from-their-own-home must sift and justify for tax purposes every expenditure of a long, arduous year. And my right-hand lady at H&R Block may not have returned from an extended leave of absence. Oh, woe! I will be spending my energies dealing with the tax status quo with not a mite left to spend on changing the “system.” I fall back on the “render unto Caesar” premise and trust that what I am rendering to God will compensate for the vagaries of the public purse. I remember that Canada had no income taxes prior to the middle of WW I. Two-thirds of what the government can do for us is based on that taxation model. When a friend wails to me that “surely the government must have a program that will help my mentally ill, homeless, drug addicted, drug-prescribed grandson,” I have to explain to her that our taxes don’t yet cover this increasingly common need and, no, the government doesn’t understand as well as we do how desperately necessary such a program is.

Laurna – I feel your pain and hope your H&R Angel reappears. And I hope that your friend’s grandson finds the help he needs. You’re right – it’s looking increasingly like a flood, and here’s us trying to shovel water with a fork.

Am I the oddball here when I say I don’t mind paying taxes? I realize that if we want to provide services there’s only one way to pay for them.

Tom

Tom – 🙂 Well, there’s no need for names… I’m more OK with paying taxes than I am with not being able to understand how they work and where they go. It seems like it should be a part of being a competent citizen.

No, you’re not. John and I feel blessed to be Canada, however flawed we imagine its tax distribution to be.

Barbara – A fair point.

Isabel – FYI with respect to the US of A.

Residents of all states are eligible to receive a federal tax credit of $7,500 for qualified EV purchases. Nineteen states offer an additional incentive beyond the federal credit ranging from a $1,000 incentive in Alaska and Delaware to a $7,500 credit in California, Connecticut, and Maine.

Contrary to a tax incentive, 24 states impose a higher annual vehicle registration fee for EVs and some hybrid vehicles to help offset forgone gas tax revenue. These fees range from $50 in Hawaii and South Dakota to $200 in Ohio, West Virginia, and Wyoming.

Five states offer both an incentive for the purchase of an EV and impose a higher registration fee for EVs than for combustible-engine vehicles. The table below summarizes details about these policies.

Another response by states to backfill reductions in gas tax collections has been to implement a tax on EV charging stations. Six recent state laws targeting EV charging stations include the following:

Georgia will require stations to track kilowatt-hour usage and collect a tax for every 11 kilowatt-hours (effective January 2025).

Iowa imposes a $0.026 per kilowatt-hour tax on public EV charging stations (effective July 2023).

Kentucky will impose a tax of $0.03 per kilowatt hour on electric vehicle power distributed by an electric power dealer (effective January 2024).

Montana imposes a tax of $0.03 per kilowatt hour or its equivalent on electric current from public electric vehicle charging stations (effective July 2023). Public charging stations already in operation have until July 2025 to install meters to collect the tax. To relieve the tax burden on in-state electric vehicle owners, B. 55 reduces electric vehicle registration fees by 30 percent starting in 2028.

Oklahoma will implement an electric vehicle charging tax (effective November 1, 2023).

Utah imposes a tax on retail sales of electric current from electric vehicle charging stations (enacted March 2023).

Just to further prove your supposition that it is complicated.

John – Thanks for this. “Too complicated for humans” seems about right: almost too complicated to understand, certainly too complicated for taxpayers to assess. At some point, you’d think they’d take a step back and ask whether there was some other simpler way to raise the money they need for the things and services we seem to want, but maybe there is not.